Features Dana

Dana is an embedded FinTech platform that generates an alternative credit score to help financial institutions (lenders) make a credit decision when you (end-user) apply for buy now, pay later(BNPL).

We are not lender, but platform to connect lender with you (end-user).Banks and Financial institutions can not finance underserved SME businesses and individuals due to the lack of credit data.

Dana helps underserved generate alternative credit score based on mobile device data and SMS transactions.

Financial institutions can make credit decisions based on Dana credit scores.

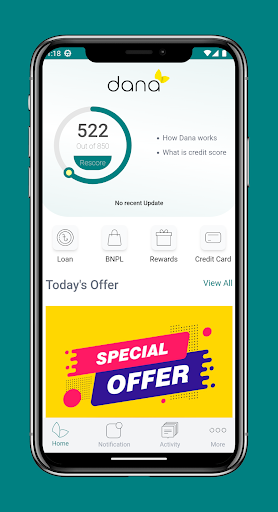

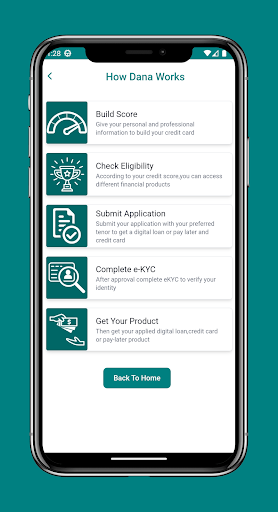

On the other hand, underbanked end-user gets access to finance through our platform.**Buy Now Pay Later**To make the BNPL process apprehensible, step by step process with an example is presented below :Jony, a student, has to build score first to check eligibility and credit limit.

Dana mobile app collects mobile device data and personal information to generate Jonys alternative credit score.

After building score , Jony can apply for BNPL within the credit limit.

Suppose, Jony gets a credit limit of BDT 20,000 BDT.

So, he can buy a product whose price is below BDT 20,000 with BNPL facility.

Then, Jony selects desired product and tenor.- Interest Rate: 8%- Processing Fee: 2%- Repayment Duration: 3 to 12 Months.Dana app shows the monthly EMI amount immediately.

For Example, Jony applied for a product worth BDT 10490 for 6 Months tenor.

Depending on the selected tenor and 8% interest rate, the monthly EMI will be BDT 1789.

After submitting the BNPL application, our partnered financial institution checks the application and approves it.

After approval, Jony has to complete the eKYC process with his Government approved ID.

The supplier delivers the product to Jony’s given address.**Credit Card**Users can apply for a credit card after building the credit score.

The user’s credit card limit will be generated based on credit score.

- Users have to give consent for the credit card limit.- Then have to complete e-KYC.- Have to give home and office addresses for verification.

- After address verification, the lender will provide the credit card to the user.****What data do we collect and why?Dana mobile app will access and process such User data, which can effectively evaluate end-users solvency and interest in obtaining financial services.SMS – Dana analyses only keywords of transactional SMS sent by financial institutions to assess end-users creditworthiness, validate income and predict repayment capacity and willingness.

Our app does not store any kind of SMS and also does not read any personal SMS.Camera – Pictures from your Devices camera.

Camera permissions to verify your identity by accessing your camera to take pictures of the ID to complete the eKYC.Storage – Storage access enables to upload of necessary documents for alternative credit scoring.How do we use and protect your data?We use user data to assess the creditworthiness of borrowers for the desired product purchase and generate credit scores.

Our partner financial institutions use Dana’s assessment in their decision process.We also use end-users data to:Obtain an assessment of creditworthiness including but not limited to an assessment of the probability of default of your obligations in the framework of contracts for the provision of financial services.Assess your interest in receiving financial services through algorithms and mathematical modeling.We securely handle all personal and sensitive user data, including transmitting it using modern cryptography (for example, over HTTPS).

We don’t use data for advertising purposes.

We will never sell end-users data to third parties.

Read our Privacy Policy on our website: [https://dana.money/privacy-and-policy](https://dana.money/privacy-and-policy)

Social Features

Connect and share with friends and the community.

Camera Features

Advanced camera features with editing capabilities.

Fitness Tracking

Track your workouts and monitor your health metrics.

See the Dana in Action

Get the App Today

Available for Android 8.0 and above